Some 5G skeptics believe 5G is risky, in terms of early deployment (perhaps all would agree 5G is a reasonable bet in a decade) because incremental new revenue is insufficient to pay for the network, or that capital investment will be too high, in relation to the revenue potential.

Those fears are reasonable enough, if more true in some markets than others, though. Consider only capital investment requirements.

If the number of cell sites to provide coverage grows by to two orders of magnitude (100 times), that has capital investment implications. Plus, many argue, all those new radio sites require backhaul or fronthaul, which means more investment on the transport network.

(Brief note, backhaul refers to the part of the network that moves traffic between the core network and the edge of the network. That includes traffic to and from the cell site or the last active network element before the subscriber location. Fronthaul is a form of “backhaul” that refers to the part of the network that moves traffic from centralized radio base stations to antenna sites. For most people, the distinction between fronthaul and backhaul is immaterial.)

Were all things equal, that expansion of cell sites would imply huge increases in capital investment, leading to a doubling to tripling of investment, some might argue. Others would say there will be an increase in capex, but only on an incremental basis (low single digits increase).

A growing number of observers might actually argue there will be flat to lower capex requirements, based on use of open source, virtualized platforms, reuse or deployment of existing assets (tower sites, fallow spectrum), plus ability to aggregate (bond, essentially) licensed and unlicensed spectrum assets, plus huge amounts of new spectrum, including lots of unlicensed spectrum or lower-cost shared spectrum.

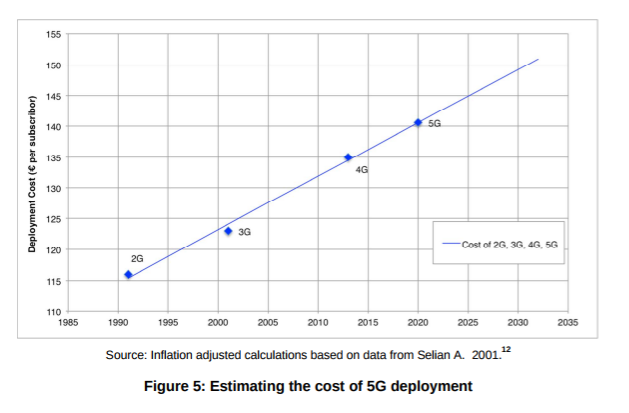

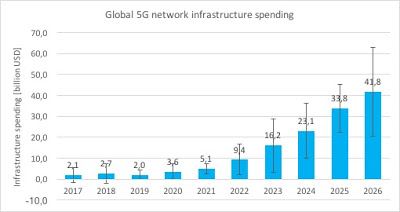

It is reasonable to expect specific 5G spending to ramp up as the networks are built. The issue, in part, is what that will cost, per tower or per potential customer. And that is where there is significant uncertainty.

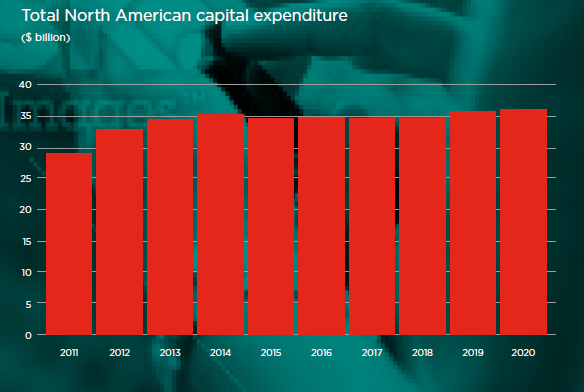

Also, tier-one service providers generally spend about the same amount, every year, on overall capex. What tends to change is the destination of that spending. And though capex climbs in the early years of a new mobile network build, that is accompanied by reductions in other areas.

The point is that firm capex tends to be relatively flat, year to year. That suggests mobile operators will find ways to keep capex within limits (as a percentage of revenue, for example). “Overall, capex for North America over the period is likely to grow slowly, slightly below the rate of revenue growth, at an annual average rate of 0.5 per cent per year between 2014 and 2020,” GSMA has said.

Skeptics will say that does not include a ramp up to build 5G, though.

Though 5G will use “all of the above” frequency assets (there will not be, as in prior networks, fixed bands to support the network), the use of huge amounts of new millimeter wave spectrum is key.

Basically, we will be able to use an order of magnitude (10 times) to two orders of magnitude (100 times) more spectrum than presently is available to support all mobile operations that had previously been unusable for technical reasons: earlier analog and digital platforms would have been too expensive.

Moore’s Law, small cell architectures, open source and spectrum aggregation (unlicensed spectrum used directly with licensed spectrum) now mean those assets can be deployed commercially.

The point is that 5G is perhaps as likely to represent incremental capex levels (“like” 4G in terms of capex) as it is to represent some hypothetical “huge increase” in capex. History suggests actual practice is more likely to represent continuity with past spending than a break with past practice (much higher investment for 5G).

No comments:

Post a Comment